Todays data

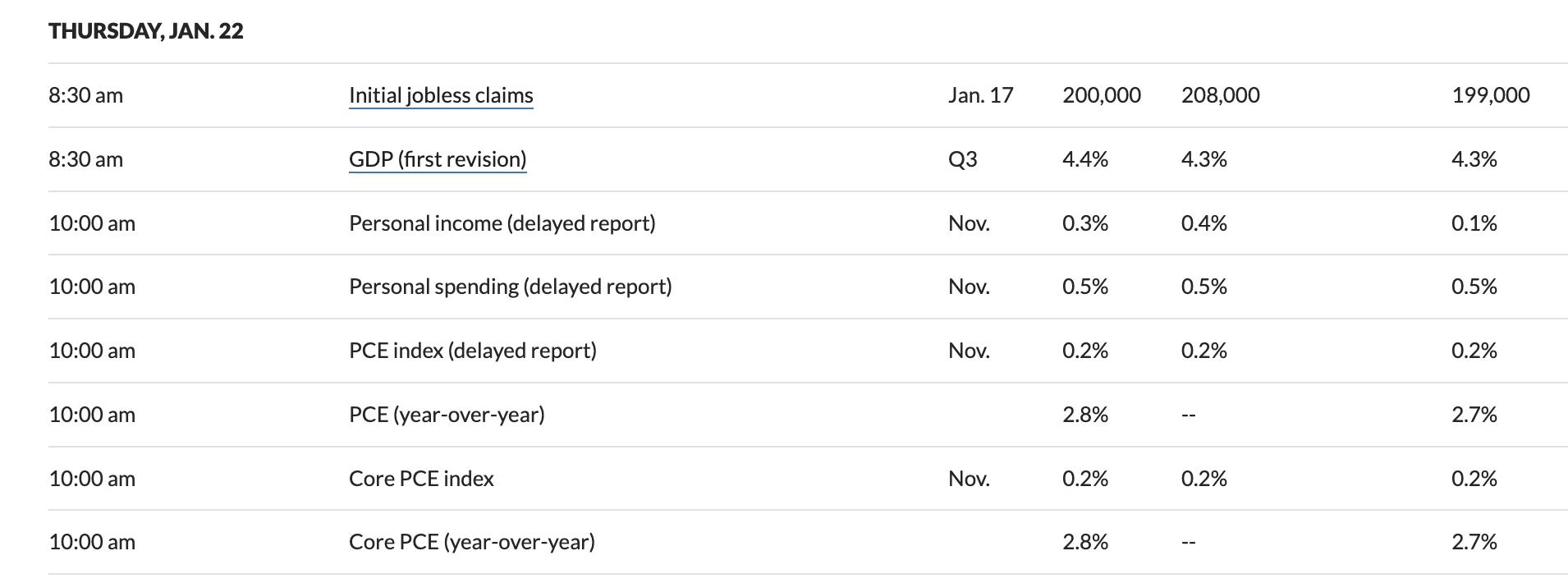

Initial Jobless claims week of January 17th

Last Read: 199k

Forecast: 208k

– Actually came in at 200k. (This is lower than expected & also a historically low number).

– The 4-week moving average was 201.5k (the lowest level since Jan 13, 2021.

– Insured Unemployment is still trending down coming in at 1.849mil

Overall the labor market is still holding together. Some economists said claims are low this year because fewer seasonal workers were hired over the holiday period. But other economists noted that non-seasonally adjusted claims are also lower.

Gross Domestic Product 3rd Quarter 2025 (revision)

Last Read: 4.3%

Forecast: 4.3%

– Real GDP actually came in at 4.4% (this is slightly to the warmer side & on track to score the fifth straight year of above-average growth).

– Was due to consumer spending, exports, govt spending, and investment. Imports (a subtraction from GDP’s calculation) decreased.

Personal Income and Outlays (this is for Oct & Nov 2025)

Personal Income:

Last read: .1%

Forecast: .4%

Actual for Nov: .3% (slightly lower)

Personal Spending:

Last read : .5%

Forecast: .5%

Actual for Nov: .5% (match)

Personal Consumption Expenditures: (both headline and core)

Last Read: .2%

Forecast: .2%

Actual: .2% monthly & 2.8% year over year. (Match across the board).

-PCE increase came from increased spending in both goods and services:

Financial services, health care, insurance, and housing & utilities. On the goods side was mainly due to recreational goods and vehicles, other non durables, and clothing & footwear.

-PCE is the feds preferred gauge of measuring inflation and this reveals inflation being stuck closer to 3% and not trending lower to the feds target of 2%.

-Here’s what people are saying about the PCE report.

The rate of U.S. inflation nudged closer to 3% near the end of last year, but probably not enough to worry the Federal Reserve or shift its main focus back to prices instead of a weak jobs market.

********My Take********

If tariffs to an extent disappear or trend lower and we see the job market begin rebounding then the “weak jobs market” worry fades away and leaves them with only the worry of inflation being stuck around 3%. (And markets want cuts????? GOOD LUCK!!)

Cutting rates eases the labor market but also allows inflation to trend higher.

As of right now, if we get a rate cut it is appearing to be June 17th 2026. That is also the first meeting with the newly elected fed chair. 46.1+12+1.1 = 59.2% chance of a cut during that meeting of 25 basis points or more. This didn’t move much after today’s data release. PCE @ expectations (close to 3%), GDP revised higher ( resilience), and Jobless Claims historically low. Is this an economy showing resilience or tightening?

Jerome Powell’s press conference on Jan 28th will be what really moves the needle on the June 17th rate cut expectations. It’s becoming more and more believed that we won’t see any cuts this year….

GDP Strong, Claims Low, Inflation Sticky: A Snapshot of the U.S. Economy

|